The Swedish “buy now, pay back afterwards” pioneer explained Tuesday that its new design would support buyers find the goods they want by utilizing extra state-of-the-art AI advice algorithms, when merchants will be able to goal prospects extra correctly.

Rafael Henrique | SOPA Visuals | LightRocket through Getty Images

Klarna on Wednesday declared a world partnership with Uber to electric power payments for the journey-hailing giant’s Uber and Uber Eats apps.

The partnership will see the Swedish money know-how agency included as a payment option in the U.S., Germany, and Sweden, Klarna reported in a statement.

In the U.S., Germany, and Sweden, Klarna will roll out its “Pay back Now” selection, which allows consumers pay off an get quickly in a person click, in the Uber and Uber Eats apps. Users will be equipped to observe all their Uber buys in the Klarna app.

The firm will also provide an additional payment choice for Uber users in Sweden and Germany which will allow buyers to bundle purchases into a one, curiosity-free payment that gets taken out of their monthly income.

Apparently, the company isn’t really rolling out installment-based acquire now, spend later strategies, arguably its most popular provider presenting, on Uber’s platforms — only quick payments and monthly payments.

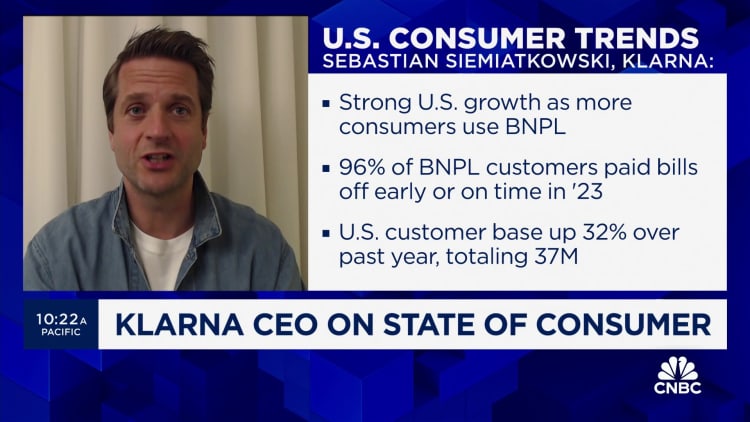

Sebastian Siemiatkowski, CEO and Co-Founder of Klarna, claimed in a statement Wednesday that the offer represented a “considerable milestone” for the corporation.

“Individuals can Pay out Now immediately and securely in total, which now accounts for over 1 third of Klarna’s world wide volumes, and far more effortlessly deal with their finances in a single position,” Siemiatkowski mentioned.

Klarna declined to disclose fiscal terms of its deal with Uber.

Large pre-IPO service provider gain

The Uber offer marks a person of the most sizeable merchant wins for Klarna of late, and will come as the European fintech giant is rumored to be gearing up for a blockbuster original public providing that could value the business at north of $20 billion.

Klarna started possessing thorough discussions with investment financial institutions to work on an IPO that could happen as early as the 3rd quarter, Bloomberg Information reported in February, citing unnamed resources acquainted with the make any difference.

CNBC could not independently verify the accuracy of the report. Klarna has reported that it would not comment on market place speculation.

These types of a industry flotation would mark something of a turnaround for a corporation that saw $38.9 billion erased from its valuation in 2022, when deteriorating macroeconomic circumstances stoked by Russia’s invasion of Ukraine triggered a reset of sky-substantial tech valuations.

Klarna reached an eye-watering $45.6 billion in a 2021 funding spherical led by SoftBank, in advance of viewing its market place value tumble to $6.7 billion the adhering to year in a so-referred to as “down round.”

The company not too long ago released a every month membership program in the U.S. to lock in “ability consumers” ahead of its expected IPO.

The solution, called Klarna As well as, costs $7.99 per month, and allows users get their support fees waived, earn double rewards factors and access curated bargains from partners including Nike and Instacart.

Previous 12 months, Klarna reported its 1st quarterly profit in 4 yrs soon after slicing its credit rating losses by 56%.

The enterprise posted running revenue of 130 million Swedish krona in the third quarter of 2023, swinging to a income for a decline of 2 billion Swedish krona in the very same period a 12 months previously.

Purchase now, pay back afterwards boom

Klarna is a person of several “buy now, pay back later on” expert services that allow users to pay out off their purchases over a period of time of monthly installments.

The payment technique has develop into increasingly well known amid shoppers to shell out for on line and in-particular person searching purchases, as an choice to credit score cards which charge interest and significant service fees.

Having said that, it has also stoked issues about the affordability of these kinds of companies, and no matter whether it is in simple fact encouraging some customers — especially young persons — to invest more than they can afford to pay for.

In the U.K., the governing administration has proposed draft guidelines for regulating the buy now, fork out later on market.

The U.S. Consumer Fiscal Defense Bureau has explained beforehand it ideas to issue invest in now, pay later on lenders to the similar oversight as credit rating card companies.

Meanwhile, the European Union past yr passed a revised variation of its Consumer Credit rating Directive to consist of acquire now, pay later products and services below the scope of the policies.

For its element, Klarna has defended the invest in now, spend later design, arguing it provides consumers a more affordable way of accessing credit score in comparison to conventional credit rating playing cards and customer loans.

The firm also claims it welcomes regulation of buy now, pay back later products and solutions.